NOL Tax Loss Carryforward

A tax relief strategy that allows businesses to use their loss in the current year in future tax years to offset taxable income

Updated:

July 16, 2023If you have your own company or are responsible for the finances of one, chances are you probably want to optimize your company's financial well-being. Therefore, you should know the different strategies available to reduce your tax liability.

One such strategy is NOL Tax Loss Carryforward, which allows businesses to use losses from previous years to offset taxable income in future years.

This tax planning strategy enables businesses to carry forward net operating losses (NOLs) from past years to offset future taxable income.

So, if you have a loss for year 1, you can use this and reduce your income in years 2, 3, 4, etc., following the loss.

This can be a complex process, where you need to understand the rules of the Internal Revenue Service (or IRS equivalent in other countries).

However, understanding the formula used to calculate NOL is an essential step in implementing this tax strategy. This involves calculating your revenue and fewer business expenses, which should result in a Net operating loss for the year.

If these accounting concepts are unfamiliar to you, consider taking the Wall Street Oasis's Financial Statement Modeling Course!

After a business has calculated its Net Operating Loss, it can carry forward that loss for a certain number of years (determined by the IRS). The rules for carrying forward are pretty complex, so business owners need to understand them to maximize their tax savings.

They also need to realize the limitations of the Tax Loss Carryforward. These include the fact that you can only use this to offset taxable income or that there is a limited carryforward period.

Also, since there are multiple ways to handle taxes and a loss, your business should consider multiple strategies to ensure this is their best option. Understanding Tax Loss Carryforward is important to any business owner's tax planning strategy.

By carefully calculating Net Operating Loss and implementing this strategy correctly, businesses can reduce their tax liability, improve their financial health, and position themselves for long-term success.

What is NOL Tax Loss Carryforward?

Net Operating Loss (NOL) Tax Loss Carryforward is a tax provision that permits businesses to use their net operating losses in future tax years to offset taxable income. NOL occurs when the allowable deductions of a business exceed its gross income during a taxable year.

The result is a negative taxable income, which allows the business to carry forward the net operating loss to future years.

The concept of Net Operating Loss Tax Carryforward can be difficult to understand, but businesses need to know about it. The provision works by allowing businesses to use their previous losses to offset taxable income in future years.

Let's pretend you have a business that reported a $100,000 net operating loss on your 10k to the IRS last fiscal year but has $150,000 in taxable income this year. The businesses can use the $100,000 loss from Year 1 to offset their tax liability in Year 2, reducing taxable income.

This is vital for businesses, especially if they have financial difficulties, as it provides them with some relief during challenging times.

For example, a business that suffers a significant loss in a particular year can carry forward the loss to offset taxable income in future years. This provision also allows businesses to plan for the future and optimize their tax liability by managing their income and expenses.

It is crucial for start-ups and small businesses that experience losses in their initial years of operation. Start-ups often experience high expenses and low income in their initial years, which can result in a net operating loss.

The ability to carry forward these losses can help them reduce their tax liability in future years and reinvest the saved funds into the business.

Net Operating Loss Tax Carryforward is a tax provision that allows businesses to carry forward their losses to offset taxable income in future years.

This is an essential provision for businesses that experience financial difficulties. It can help them optimize their tax liability, allowing for better tax planning decisions and improving their overall financial situation.

How do you calculate NOL Tax Loss Carryforward?

Calculating Net Operating Loss (NOL) is essential for using Tax Loss Carryforward. It has its formula, using the business's gross income & deductible expenses.

The formula for calculating Net Operating Loss is as follows:

Net Operating Loss = Gross income – Deductible expenses

Gross income is the business's total revenue for its fiscal year. Deductible expenses are business expenses that can be subtracted from gross income to get taxable income. These expenses include rent, salaries, COGS, and depreciation & amortization.

Let's pretend we have a small retail store with a gross income of $500,000 but $600,000 in deductible expenses. The calculation for Net Operating Loss would be as follows:

NOL = $500,000 – $600,000 = -$100,000

This means the business had a Net Operating Loss of $100,000 this fiscal year.

Calculating NOL can vary for different types of businesses, depending on their structure and how they account for income and expenses.

For example, sole proprietors and partnerships calculate NOL using the same formula mentioned earlier.

However, corporations use a different formula to calculate Net Operating Loss, considering their capital losses, dividends received deductions and other factors.

Moreover, for businesses that use accrual accounting, Net Operating Loss is calculated based on when the expenses and revenue are incurred, regardless of when the payment is made.

In contrast, cash-basis accounting records expenses and revenue based on when they are paid.

Calculating NOL is a critical step in utilizing Tax Loss Carryforward. The formula for calculating Net Operating Loss considers a business's gross income and deductible expenses.

The calculation of NOL may vary for different types of businesses, depending on their structure and accounting methods. Businesses must understand how to calculate their loss accurately to make the most of the Tax Loss Carryforward provision.

How to Carry forward NOL?

Carrying forward Net Operating Loss is crucial in utilizing the Tax Loss Carryforward provision. However, businesses must follow specific rules and regulations to carry the loss forward.

One of the essential rules for carrying the loss forward is that it can only be carried forward to future tax years, not backward. Therefore, businesses cannot use it to offset taxable income in previous tax years.

However, they can carry it forward for up to 20 years after the year in which the loss occurred. This means businesses have considerable time to use their NOL to offset taxable income in future years.

Another important rule for loss carrying forward is that it must be carried forward in a specific order. For instance, the oldest Loss Carryforward must be used before the newer ones.

Also, your net operating loss cannot offset more than 80% of the company's taxable income in the future. Any remaining loss can be carried forward to the following year until the 20-year limit is reached.

To use your net operating loss benefit in future years, your business must submit an application to the IRS. The application must include a statement showing the computation of the NOL, the year it was incurred, and the amount being carried forward.

The IRS will then verify the loss and provide a certificate of carryforward, which the business can use to offset taxable income in future tax years.

It is essential to note that certain limitations and exceptions may apply to carry forward your net operating loss.

For example, if the business has an ownership or structure change, the carryforward loss may be subject to limitations or restrictions.

Businesses can carry forward loss for up to 20 years after the year in which the loss occurred, but it must be carried forward in a specific order and used to offset up to 80% of taxable income in a future tax year.

To apply NOL to future tax years, businesses must file an application with the IRS, which will provide a certificate of carryforward. Businesses must understand the rules and limitations of carrying forward NOL to make the most of this tax provision.

Advantages & Disadvantages of NOL Tax Loss Carryforward

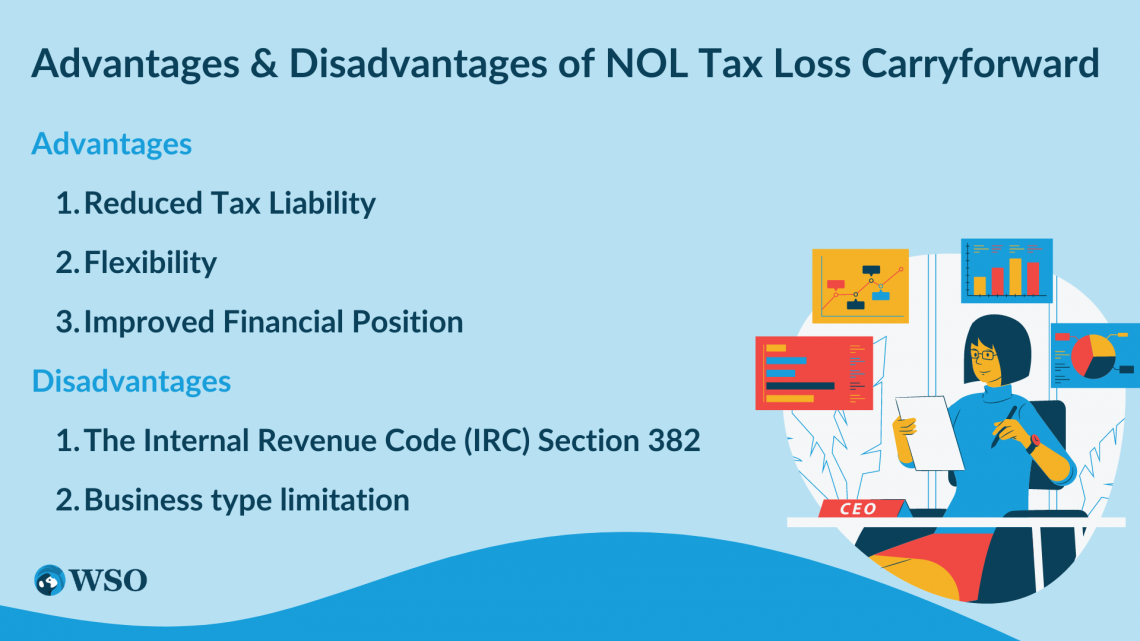

While NOL Tax Loss Carryforward is a valuable tax provision for businesses, businesses must be aware of several advantages and limitations on its use.

The advantages are:

1. Reduced Tax Liability

Allows businesses to offset taxable income in future tax years, thus reducing their tax liability. This, in turn, helps to conserve cash for the business.

2. Flexibility

It gives businesses flexibility when adjusting tax strategies based on their financial situation. For example, suppose a business experiences a loss in one year. In that case, it can carry forward that loss to future tax years and offset future taxable income.

3. Improved Financial Position

Businesses can reinvest and improve their financial position by conserving cash when they reduce their tax liability. The Tax Loss Carryforward is a valuable tax provision, but businesses must understand several limitations on its use.

These limitations can significantly impact a business's tax planning and tax liabilities, and businesses must carefully plan their tax strategies while considering these limitations.

Some Disadvantages are:

1. The Internal Revenue Code (IRC) Section 382

If a business undergoes a change in ownership, the carryforward loss may be subject to limitations or restrictions.

It can only use its NOL to offset taxable income up to the value of the business's assets at the time of the ownership change multiplied by the long-term tax-exempt rate.

This limitation prevents companies from acquiring loss-making businesses solely to use their NOL to offset taxable income.

2. Business type limitation

Certain types of businesses, such as farming businesses and certain regulated investment companies, are subject to special rules and limitations regarding using NOL.

For instance, farming businesses may carry forward for up to 20 years, but they can only use it to offset up to 100% of taxable income in a future tax year.

The amount of taxable income is another limitation on the use of NOL. As per the IRC Section 172, businesses can only use their loss to offset up to 80% of taxable income in a future tax year.

Let's say a business has a net loss of $100,000 and a taxable income of $150,000. This means you can only use $120,000 to offset taxable income.

In practice, these limitations can significantly impact a business's tax planning and tax liabilities. For instance, if a business changes ownership, it may lose a significant portion of its Carryforward loss.

Similarly, if a business has substantial taxable income, it may not be able to utilize it entirely. Therefore, businesses must carefully plan their tax strategies while considering these limitations.

Factors to Consider

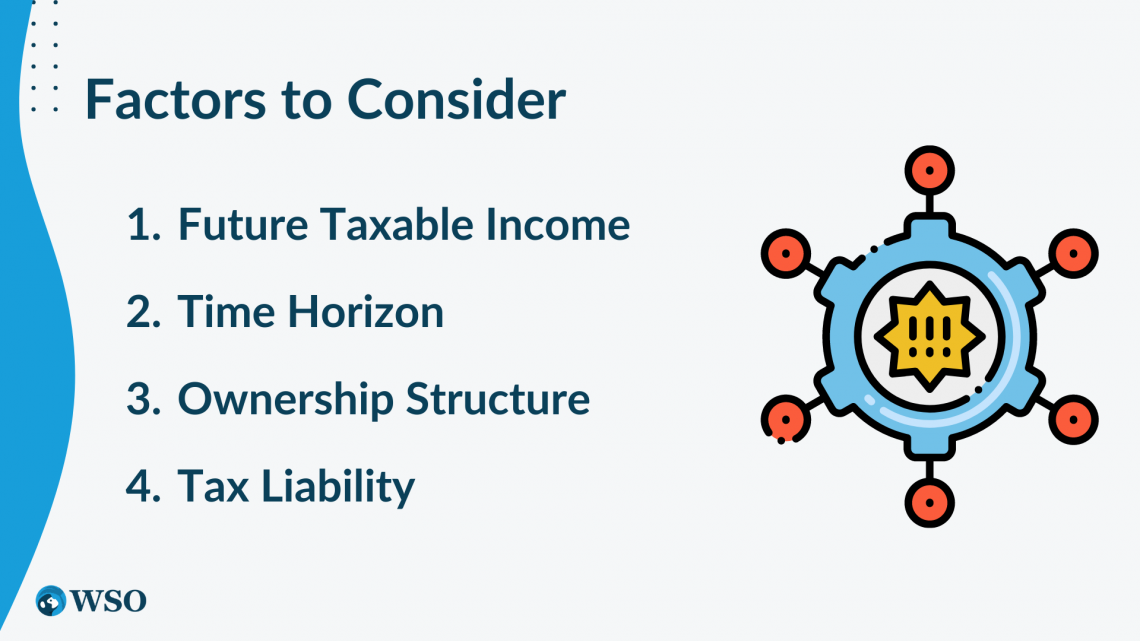

To determine if tax relief is the right strategy for your business, you should consider the following factors:

1. Future Taxable Income

It may be viable if you expect to generate positive income in future years.

2. Time Horizon

If your business has a long future, it may be beneficial as you can carry the relief forward.

3. Ownership Structure

If your business goes through a change in ownership, this strategy would have limitations or restrictions.

4. Tax Liability

If your business has a significant tax liability, this can help reduce the tax liability and conserve cash.

Tax Loss Carryforward can be a useful tax planning strategy for businesses, but this tax provision has advantages and disadvantages. To determine if Net Operating Loss Tax Loss Carryforward is the right strategy for your business, you should consider factors such as

- future taxable income,

- time horizon,

- ownership structure, and

- tax liability.

By carefully considering these factors, you can make an informed decision about utilizing Carryforward for your business.

NOL Tax Loss Carryforward vs. NOL Tax Loss Carryback

Loss Carryback is the counterpart of Loss Carryforward. The Tax Carryforward allows businesses to use their losses on future taxable income, while the Tax Carryback allows businesses to attribute losses back to the last 2 years.

| NOL Type | Carryforward | Carryback |

|---|---|---|

| Time Limitation | Allows you to carry tax loss relief forward. | Allows you to attribute the tax loss relief to the last 2 years. |

| Cash Flow | Helps to conserve cash for businesses by reducing their tax liability in future tax years. | Provides businesses with a cash refund of taxes paid in previous tax years. |

| Risk | Less Risky. | Carries more risk. If a business carryback its losses and has taxable income in the carryback year, it may end up paying more taxes than without it. |

Which strategy is better for your business?

The decision to use Carryforward or Carryback depends on the specific circumstances of your business.

- Suppose your business expects to generate taxable income in future tax years. In that case, Loss Carryforward may be the better strategy, as it allows you to offset that taxable income with the carried forward losses.

- If your business has paid taxes in previous years and has losses in the current year, Carryback may be a better strategy, as you could get a tax refund.

Summary

Net Operating Loss Tax Loss Carryforward is a tax relief strategy that allows businesses to use their loss in the current year in future tax years to offset taxable income.

This relieves them of financial distress, which can help them pay fewer taxes in the future. In essence, Tax Loss Carryforward enables businesses to carry forward losses they incurred in previous years to offset their taxable income in future years.

Calculating NOLs is an essential step to make use of Tax Loss Carryforward. Net Operating Loss can be calculated by subtracting a business's deductible expenses from its gross income in a particular tax year.

If the result is negative, the business incurs a net operating loss. This loss can then be carried forward to future tax years to offset taxable income, thus reducing the amount of tax payable.

There are limitations to the use of Tax Loss Carryforward that businesses should be aware of, like the 80% limit on the amount that can be offset and restrictions based on the type of business entity.

Tax Loss Carryforward can be a useful tax strategy for businesses that have experienced losses in previous tax years. Still, you should consider all of its limitations & restrictions before using this strategy.

Understanding the ins and outs of Tax Loss Carryforward can help businesses avoid costly tax mistakes and improve their overall financial situation.

NoL Tax Loss Carryforward FAQs

NOL Tax Loss Carryforward is a tax provision that allows businesses to use their net operating losses in future tax years to offset taxable income.

Net Operating Loss is calculated by subtracting a business's deductible expenses from its gross income in a particular tax year.

The CARES Act passed in 2020 temporarily increased the carryforward period to five years for losses incurred in tax years beginning in 2018, 2019, and 2020. In general, businesses can use carry forward up to 20 years.

Most businesses can, including corporations, partnerships, and sole proprietors.

No, it cannot be transferred or sold to other businesses. Instead, each business must use its loss to offset its taxable income.

Everything You Need To Master Financial Statement Modeling

To Help You Thrive in the Most Prestigious Jobs on Wall Street.

or Want to Sign up with your social account?