Current Liabilities

Understood to be settled within one financial year or an operational cycle.

Updated:

August 16, 2022The term "liability" suggests that a person or company owes goods/and or services to another person or business. In accounting, current liabilities are understood to be settled within one financial year or an operational cycle.

Liability, in simple terms, means some product or service or cash that you know to another person. An example might be mowing the lawn after the homeowner paid you beforehand. Since they paid you prior, you are liable for completing the service of mowing the lawn.

They are also short-term liabilities as they have to be settled within a short period. Usually, anything under a year is considered short-term.

There is also a liability such as non-current liabilities, which are long-term settlements. Any settlement(s) to be paid longer than a year is considered a long-term liability. Usually, these could last from 2-3 or even 15 years.

They are mostly settled by liquidating existing assets but can also be determined by replacing the liability with another liability. For example - a company has to pay off a recent payable (a.k.a a liability) and chooses to pay it by taking out another loan (a liability) from a bank.

The types of liabilities can widely range. It mostly depends on what sector or industry a company works in,

Some examples include:

- Accounts payable

- Short-term loans

- Income Taxes

- Dividends

- Notes payable

Current liabilities give investors or banks insights into a company's financial strength.

Investors and creditors both benefit from a thorough examination of current liabilities. Banks, for instance, like to see firms collecting payments through their accounts receivable before deciding to issue them a loan.

In case of high current liabilities, a company should allocate its resources efficiently, which may mean job redundancies, optimizing operations, and shifting internal controls. More often, this is where consulting firms like the Big 4 (K.P.M.G, Deloitte, E.Y, and P.w.C) come in.

The consulting firms help a company identify a problem, diagnose the core area, and find, create, and implement a solution to achieve the desired result (in this case, reducing current liabilities).

Where are Current Liabilities recorded? Where are they found on a Financial Statement?

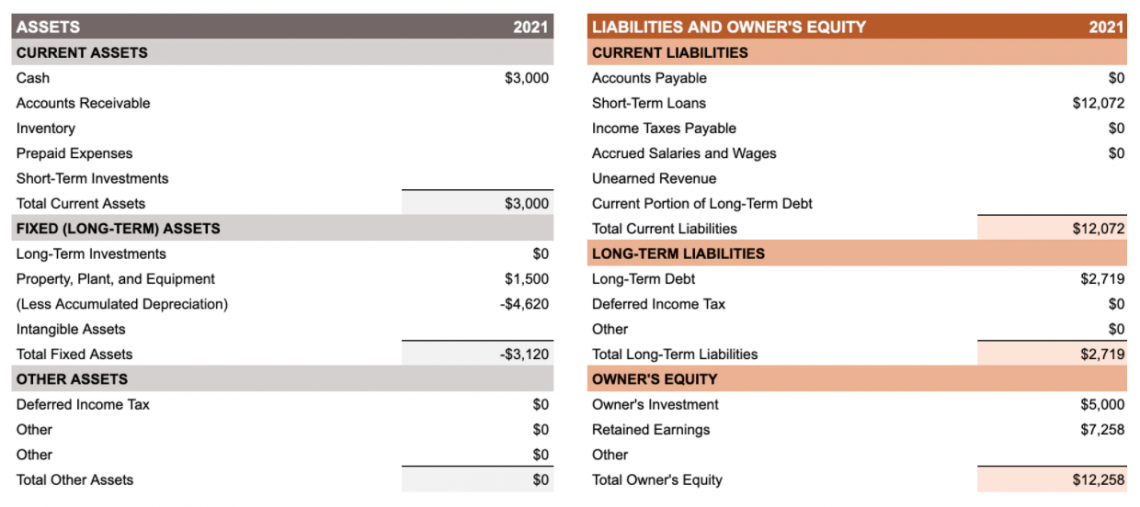

A balance sheet or statement of financial position is a document given to a company's concerned groups (concerned groups are just banks, investors, creditors, etc., who want to see the health of a company).

The document shows the financial position of a company and displays what the company owes and owns.

The principal formula for the balance sheet is:

With the efficient use of data provided in the balance sheet and income statement, a few factors can be assessed, such as liquidity, efficiency, rate(s) of return (R.o.R), and leverage. Current liabilities are stated under the liability column on the balance sheet as shown below:

The "Liability and Owner's Equity" column consists of 'Current Liabilities,' 'Long-Term Liabilities,' and 'Owner's Equity.' Out of these, we will be discussing 'Current Liabilities.'

The transactions are recorded by crediting the most applicable current liability account and a debit to an expense or asset account in double-entry bookkeeping.

For example, a person purchases a brand-new laptop worth $2,000 for his e-commerce business. Then, he transfers $2,000 from his cash account to his expense account. This is because he has less cash in hand and his technological expense assets are now worth $2000 more.

The software most commonly used for making these financial statements and modeling is Microsoft Excel.

Ratio & Analysis

Ratio Analysis is really helpful for a business to help determine their performance statistics against the industry or sector they compete in.

Analyzing ratios also provides insights into a business:

- Solvency

- Liquidity

- Operational efficiency

- Profitability

Which helps the business gauge and work to become more competitive in the market.

These ratios are derived (or calculated) from the items listed on the balance sheet & income statement.

The Current Assets ratio shows a business's current assets to its current liabilities as shown in the formula below:

The current ratio is a liquidity ratio that measures a company's capacity to pay off all its present liabilities due in one fiscal year.

A good current ratio determines the wealth of a business. A current ratio of around 1.5 to 3 is considered an indicator of a good profit-making business.

An efficient analysis can highlight the problems or other issues in the business. However, the limitation of ratio and analysis is that they help identify the problem but not the solution.

Similar to the current ratio, another ratio known as the acid test Ratio (Quick Ratio) helps determine the liquidity of assets in a business. The formula for the acid-test ratio is shown below:

This ratio can also be calculated from the resources provided on the balance sheet. A normal Acid test ratio for a business should be 1:1 or higher.

The higher the acid test ratio is, the liquidity of a business increases.

The cash ratio is the most commonly used method to determine a business's liquidity. If a company is to pay off all its current liabilities, this metric shows its ability to do so without liquidating or selling other assets.

The formula for the cash ratio is:

![]()

There is no ideal figure for a 'normal' or 'good' cash ratio, but if the cash ratio is between 0.5 to 1, it is considered a good cash ratio.

For example, a company having $200,000 in cash and marketable securities and $150,000 in short-term liabilities would have a cash ratio of 1.33, which would be considered a great cash ratio.

Calculation :

Cash Ratio = $200,000/ $150,000

Cash Ratio = 1.33

Current liabilities vs. Non-Current liabilities

Other than funding day-to-day operations, a company also raises money for various capital expenses from time to time. These include fixed assets and property acquisitions.

Capital expenses are usually funded through long-term liabilities, such as bank loans, public deposits, bonds, debentures, and deferred tax liabilities.

Few Current Liabilities Discussed below are

Bank Overdrafts - Overdrafting is a commitment that lets you utilize money in your current account by taking out more money than you have. It is considered a liability to be paid within 12 months since interest is charged.

*Remember, anything under a year is considered a short-term loan.

Bank overdrafts are a liability because an excess amount is taken beyond the available funds in your account, leaving your account in a negative balance. Moreover, there are two types of bank overdrafts - authorized bank overdrafts and unauthorized bank overdrafts.

Authorized bank overdrafts - Advance arrangements made between the account holder and the bank. Both parties agree mutually on a limit that can be used on any payment that might take place in the future.

Advantages of having an authorized overdraft -

- Fulfilling an urgent cash requirement

- Interest is to be paid only on the amount to be utilized

- No requirements for collateral

- Availability of cash for a business or an individual

Unauthorized bank overdrafts - No advance arrangements are made between the account holder and the bank when the account holder spends more than deposited.

An "unauthorized" overdraft occurs when you go overdrawn without first getting the bank's approval. Your credit score could be impacted by this, making it more difficult for you to obtain credit in the future.

Current portions of loan borrowings - Current Debt is also known as short-term debt or the current amount of long-term debt as it is a short-term obligation.

Current debt includes formal borrowings of a company outside account payable and has to be paid off within one financial year.

For example, a company pays machinery costs in installments.

Current debt and capital lease obligations are both liabilities on a balance sheet. As a result, some firms call these Notes payable. This is different from accounts payable, which include goods and services, whereas notes payable relate solely to borrowed cash or funds.

Trade and other payable - Accounts payable include the money owed by businesses from their suppliers for products/services purchased on credit. It includes monthly bills, rents, and other miscellaneous expenses.

Account payable is a burden on the company's shoulders.

The repayment period for the account payable can differ depending on the product or service from weeks to months. Usually, the repayment period for accounts payable is a few months.

Disadvantages -

In case of a delay in payments, there is pressure on the supplier's financial position. Therefore, suppliers tend to give the business a shorter credit payback period (shorter amount of time to pay) for payments.

Prolonged accounts payable reflected in financial statements can forecast the company's financial trouble.

Any delay in payments can impact the relationship between a supplier and business and, thus, potentially harm long-term business relationships.

Provisions: These are funds set aside by a business to cover any future losses. In other terms, a provision is an obligation whose timing and magnitude are unpredictable. On a company's balance statement, provisions are shown in the liabilities section.

Provisions include warranties, income tax liability, future litigation fees, depreciation costs, guarantees, pensions, losses, asset impairments, provisions for bad debt, etc. Provisions are not a form of savings as the expense is likely to occur.

Provisions account for certain company expenses and payments for the same year. These make the company's financial statements more accurate and precise.

Eligibility to be a provision means that the capital should be for a specific purpose, and the obligation should be at least a probability of 50%.

Dividends Payable (liability dividend) - A liability dividend is a promise to shareholders to pay them their dividends at a later date. It is insured when a company faces liquidity problems and does not have the cash to pay its shareholders in the near term.

The receiver of a liability dividend can choose either to wait until a later date to collect dividend distribution or sell it to a third party at a discount rate.

When a dividend is declared, it is recorded on a company's financial records and reported on its balance sheet.

Young startups tend to reinvest dividends to grow their company via scalability and expansion. In contrast, mature company dividends are enjoyed by shareholders as the company has reached optimal levels of growth and scalability.

The regular distribution of earnings also makes the company a good fit for investments in the eyes of certain investors who want a periodic income stream from their stock investments.

- All liabilities must be settled within one financial year or operating cycle-current liability of various debts, payable, etc.

- The current liabilities are stated under the liability column on the balance sheet.

- A corporation's time to purchase inventory and convert it to cash from sales is referred to as an operating cycle.

- Ratio and Analysis are really helpful for a business to help determine their status in the industry or sector. The current acid test and cash ratios are a few important ratios discussed.

- They are to be settled within one financial year, whereas non-current liabilities have more than one year term for settlement.

- They are usually settled with current assets, which are assets that are consumed within a year.

- They include dividends payable, provisions, trade payable, current portion of long-term debt (short-term debt), and bank overdraft.

Everything You Need To Master Financial Statement Modeling

To Help You Thrive in the Most Prestigious Jobs on Wall Street.

Researched and authored by Abhinav Bhardwaj | LinkedIn

Free Resources

To continue learning and advancing your career, check out these additional helpful WSO resources:

or Want to Sign up with your social account?